A friend recently pointed out the depth and scope of evil that we humans are capable of commiting, referencing Auschwitz and another person pointing out the savage brutality at Jasenovac concentration camp. They were fathers, mothers, police officers and even priests that committed such acts of extreme violence and genocide. These examples and many other ruthless crimes against humanity from across the globe are stark reminders that we still have a long way to evolve and given the right circumstances, we are still susceptible to descending into the brutal mass murders utterly devoid of empathy and compassion.

There are several ways we can mitigate or counter such dangerous torrents of history. I’ve introduced OICD’s work about countering identity weaponisation and explained ways in which narrowing of identity can be manipulated through propaganda. When we begin to consider the role of modern divisive technologies in fast-tracking such malevolent ambitions, their work may prove to be a critical component in maintaining peace in the coming decades. I’ve also explained in detail, ways of strengthening communities that could create resilience and safeguard against social division and misuse of power which feels more and more relevant in the wake of the current social unrest in the US.

But this time, I’d like to cover the basic grounds on what part a deep financial crisis plays since they have often acted as a prologue to fascism. By understanding how runaway inflation affects our lives and by placing a few strategies to protect ourselves, we may be able to curb the degree of damage and slow the sinister transformations in the political will.

Fascism rose to power by taking advantage of the political and economic climate of the 1920s and 1930s, particularly the deep polarization of some European societies, which were democracies with elected parliaments, whose intense opposition to each other made it difficult for stable governments to be formed. Fascists used this situation as an argument against democracy, which they viewed as ineffective and weak. Fascist regimes generally came into existence in times of crisis, when economic elites, landowners and business owners feared that a revolution or uprising was imminent. Fascists allied themselves with the economic elites, promising to protect their social status and to suppress any potential working class revolution. In exchange, the elites were asked to subordinate their interests to a broader nationalist project, thus fascist economic policies generally protect inequality and privilege.

https://en.wikipedia.org/wiki/Economics_of_fascism

Inflation

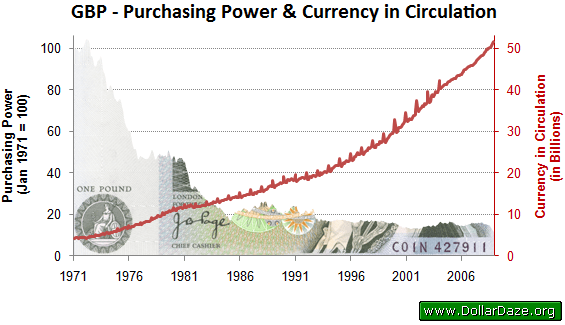

One key idea that is central to understanding the current global trend is how our central banks and governments are able to ‘create’ an unlimited amount of currency by borrowing it into existence. To understand how this affects the prices of items, it is helpful to lay out the fundamentals of pricing. Less currency in circulation means that there is less currency chasing the same number of goods, therefore the prices of items begin to drop (or more accurately, the value of the currency increases). More currency in circulation means that there are more of it chasing the same number of goods which raises the prices of items (it takes more currency to buy the same goods and services, meaning that the value of currency has decreased).

Most consider 2 to 4% annual inflation to be a healthy sign of growth but consider this; in 100 years averaging 3.9% inflation, the same items which cost £10 in 1920 now cost £450. The value of the item hasn’t changed but the currency you’re using to pay for it has diminished in value as a result of more currency being pumped into the economy over time. To put it simply, the central banks and the government’s currency printing dilutes and steals the purchasing power from our savings and gives it to the first people who spend it. Even if your bank pays interest on your savings – say 1.5%, if it is lower than the rate of inflation – say 3%, your savings are being devalued by 1.5% annually.

Another effect of inflation worth considering is that people who already own assets will benefit from the effects of inflation, while those who don’t will find it harder and harder to afford it. Take real estate as an example, if your grandparents bought an average house in the 1960’s it would have set them back £2530 when the annual salary was around £960. So roughly 2.5 times your annual salary. The same property may have risen in value to over £200,000 in today’s market while the average salary stayed low at £27,600, making the price of average homes 7 times your annual income (discounting ultra-high earners skewing the statistics, probably 8, 9, 10 times for many properly average people like me). This perpetuates wealth inequality since those who already own homes become vastly richer while those without are squeezed out of the market.

We are currently seeing unprecedented money printing across the globe (at the expense of our taxes, the dilution of our savings and by binding the future generations to debt repayment) with the large majority of it ending up in the financial market pushing the stock prices artificially higher while unparalleled levels of unemployment rages on. In America, based on a 2016 data (so likely far worse now) the wealthiest 10% owned 84% of stocks while the bottom 80% owned 6.7%, meaning that the rise of value in the stock market we are seeing right now disproportionately enriches the likes of Bezos, Musk, Zuckerberg and Gates. The richest become even richer while the poorest are left struggling to pay for their basic needs.

Hyperinflation

A lot of economics is about human psychology. One of the outcomes of the current Covid-19 pandemic is that it has switched the general collective psychology from debt-fueled consuming spenders to savers – meaning that a larger percentage of currency in circulation now sits dormant in bank accounts reducing what’s called the ‘velocity of money’. It’s been discussed widely that once the virus subsides and people feel secure in the amount they’ve saved or more confident in the future economic outlook, the savers become spenders again and prices will begin to inflate. The prediction of this timing varies widely from 2 to 10 years dependent on multiple factors such as the speed and efficacy of vaccines, the amount and distribution of monetary stimulus, global geopolitical tensions etc.

With billions and trillions being printed, at some point, usually after a period of adjustment, prices eventually begin to catch up to account for all the extra currency created. The speed of price inflation wakes up the general public to the fact that a £10 note that you have in your wallet may buy far less a month, a week, a day from today and will push people towards spending it to get rid of the rapidly devaluing currency, accelerating the vicious downward spiral in the process as hoarding and shortages drive up prices further.

When we see a minimum 50% increase in inflation within a month, we are in hyperinflation. This means that a loaf of bread that costs you £1 at the beginning of the month will cost £1.50 at the end of the month. £2.25 by the end of the next month, and £144.12 by the end of the year. Zimbabwe in 2008 had prices doubling almost every 24 hours and Venezuela is currently in the midst of extended hyperinflation with a rate of 10 million percent since 2018, while blackouts, food and medicine shortages and the largest exodus in Latin American history continues on. We may see large scale famine and anarchy unfold in Venezuela in the coming years.

When the pensions and savings of the middle class are wiped out in a matter of months, weeks and days as in the examples above, history shows that many will begin to blame their pain and destitution on ‘others’ and vote in pathological monsters who provide a scapegoat and promise ‘solutions’ which could and have descended into rein of pure evil.

Some Possible Safeguards

So how do we protect ourselves and those around us from such a catastrophic future? One way is to preserve the wealth of the middle class and the poor by creating a safeguard against the destructive forces of hyperinflation. This could be done by turning your savings, which for many are in their respective fiat currency, into something tangible and useful. I have been slowly buying things that I’ve always wanted but held off for a while, which will last a long time and be useful in times of scarcity. I am planning on buying some really high-quality gardening tools and other equipment that will facilitate resilience too. I am actively searching for a plot of land so that I can plant an orchard and grow food, not only for myself but for the surrounding community. These are assets that once purchased, become detached from the market forces and retain their value over time.

1971 marked the end of the Bretton Woods system which tied the currency to gold. This began the new age of fiat currency where it was no longer tied to something inherently limited in quantity, meaning that people in power were now able to print as much as they wanted. There are other charts on this website that graphically illustrate so much of what’s wrong with our current system stemming from that decoupling from physical, tangible store of value – gold. https://wtfhappenedin1971.com/

When your savings begins to lose its purchasing power day by day, hour by hour perhaps even minute by minute, the rush to assets that acts as a store value becomes accelerated. Over the five years of Weimar hyperinflation, gold increased in value 1.8 times faster than the inflation rate, meaning that people holding gold came out of the inflation nearly doubling their purchasing power while everyone else lost their savings. With the interconnectedness of the global economy, coupled with so much more currency in circulation and a far greater number of wealthy investment minded populations across the globe, I’m expecting the value of gold, silver and crypto to increase many many times more than it did in the 1920’s.

I used to think that going back to a gold standard, where real money was limited in supply, was the best solution to the problems we have in the economy. But Galgitron’s point in this post changed my mind. He notes that even with a gold standard, “the rich would still systematically get most of the gold, but there’s no way to easily redistribute gold. Trust me when I say, when choosing between a gold standard (no reset) or fiat inflation (quasi-reset), we’re much better off with fiat.” A truly dystopian perspective that makes a lot of sense given the current systemic flow of economic capital from the poor and the middle class to the super rich. I will be looking closely at what China and Russia will do with the gold they have hoarded in the last decades.

We may also see some enormous moves on crypto as they are designed to replicate the scarcity of precious metals and remain transparent and free from government manipulations. But countries like China and Russia are planning to roll out their own government issued cryptocurrency. This is something we must be fearful of and act decisively against. Allowing our governments to control our money can lead to serious long-term consequences. If not the current leadership, someone down the line will misuse the power to freeze and seize your account if they assume you are a risk to their political power. In addition to controlling your money, they may be able to trace your every purchase, have access to a lifetime of data and will be able to set boundaries of where and what you can use the currency for.

My Strategy

So to sum up, I think the best option left for us is to understand how the rigged financial system works and play the game like an insider. For 12 years since the 2008 crash, I’ve been studying how the economy works and began following the moves of successful investors that are aware of the fundamental forces and applied my tiny savings in a similar way. I am currently positioned in physical gold, silver and crypto. I see this as the only way to obtain a plot of land without going into 30 years of debt slavery. Note that I am not a financial advisor so don’t take my word and do your own research. Many people allocate a small percentage of their wealth in precious metals and crypto as a hedge against inflation and the decision is up to you what you feel is the best protection against things to come.

Update: I’ve increased my crypto holdings in October 2020 to about 50% with more news of institutional investors moving in. I’ve been learning about this new emerging ecosystem and have converted the rest of the precious metals into it as my strategies and information sources became more and more refined. I still think gold and silver are the safer bet and I wouldn’t recommend jumping into crypto at this overheated stage without doing proper research and have a solid exit strategy.

I’ve disclosed my strategy in detail because I feel that barriers to land ownership is the biggest bottleneck to the sustainability movement. Many of those wishing to live within the means of nature, with the intent of regenerating land and increasing resilience against future catastrophes are often unable to afford the current price tags. But these outlined strategies that ride the waves of wealth transfer cycles are a fairly reliable way of getting around it. And for poor people with a little bit of savings, riding these volatile times correctly has the potential of turning it into a once in a lifetime opportunity. So follow the links, read up, watch videos and position yourself to gain from the unfolding crisis. With more people protected, we can massively diminish the chances of history taking a darker turn.